With IRS revisions, which are increasing in 2025, cryptocurrency holders are facing more control than ever. It’s not just about paying taxes. The developing rules mean that even small supervision can lead to large sanctions or expensive audits.

You read Crypto Long & Short, our weekly newsletter with insight, news and analysis for the professional investor. Sign up here to get it in your inbox every Wednesday.

Below are five common mistakes that often catch cryptoinvestors away – and how to remain compatible.

- Neglecting wallet -based accounts: The IRS now expects detailed reporting of each wallet transactions and balances. It doesn’t mean clumping all your trades together on a single spreadsheet. Whether you use hot wallets, cold wallets or a combination of both, each wallet’s records must be traced individually. Tools such as Cointracking, Coinledger or Taxbit can simplify this process by syncing real -time data from different exchanges. Proper wallet -based accounting not only keeps you compliance, but also prevents surprises if the IRS decides to dig into your transaction history.

- Misreporting Stack Redes: POINTING REWARDS is taxable income as soon as they hit your wallet – even if you haven’t sold them to Fiat. Many people mistakenly believe that they should only report income at the time of sale, but the IRS disagrees. For example, if you earn 2 ETH to a value of $ 3,000 in total by inserting rewards, the taxable income when received. Missing or wrongly these amounts may draw unwanted attention from regulators that already see crypto activity closely.

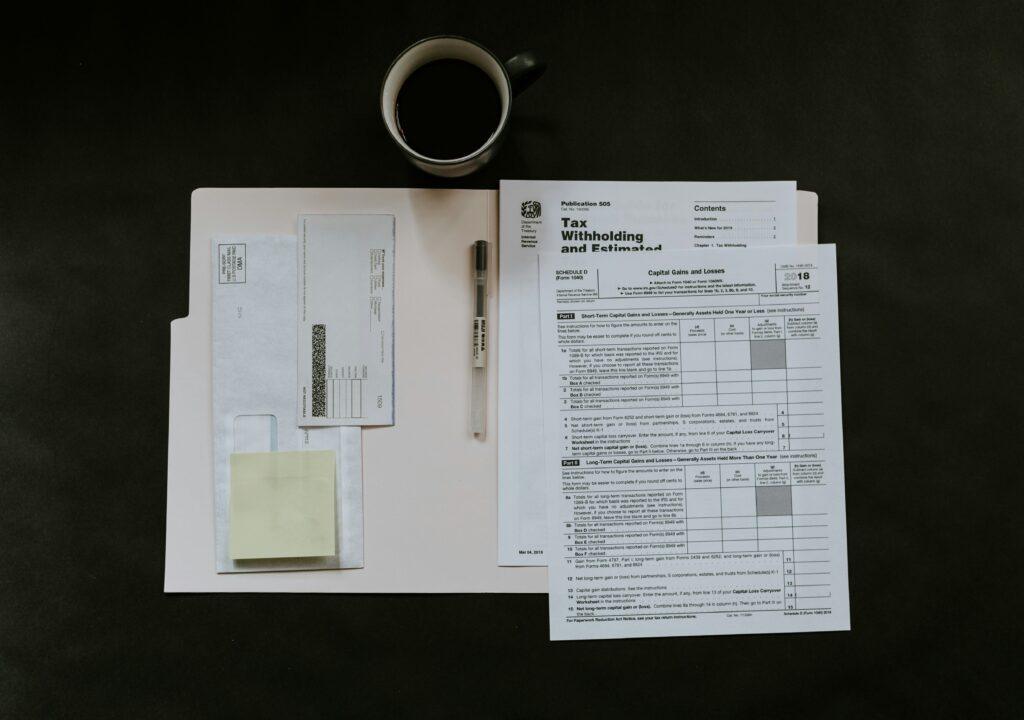

- Overlooking IRS letters and form 1099-da: Key IRS messages such as message 6371 (basically “We have questions”), Message 6374 (“Explain yourself”) and CP2000 (“We think you owe us”), can arrive if something does not match your tax reports. In 2025, Crypto Exchanges also sends form 1099-when outlining your crypto income, trades and rewards. Any discrepancy between this form and what you report is a Surefire Red Flag. Always review these documents carefully for accuracy and be prepared to correct any errors before escalating.

- Failing to report all transactions: Do you think the little ones trades on a decentralized exchange are invisible? Think again. IRS and its partners have sophisticated blockchain analysis tools that track activity, even on decentralized exchanges (DEXS) and privacy coins. Each transaction – trades, air drops, forks and rewards – must be included in your tax archiving. “I forgot” won’t save you if your drawing addresses are linked to non -reported transactions.

- Missing the chance to adjust the cost basis and avoid excessive deductions: The tax year 2025 brings a critical opportunity to adjust your crypto cost base according to new guidelines. These rules allow investors to redistribute unused cost base across wallets or exchange accounts, provided they document the method before their first 2025 trade and follow specific registration requirements. Performed correctly, it can lower your capital gains tax and keep you in the clear. To go too far with a deduction-as inflation of business expenses or hobby-related costs can trigger a revision if the number seems unrealistic. The IRS controls deductions that do not match typical income levels, so stay within land and maintain thorough supporting items.

Become ready for audit

Crypto taxation is increasingly complicated, but staying compatible does not need to be stressful. The best practice? Use reliable crypto-tax software, double control of any detail of your return, keep careful items and be transparent if you detect previous errors. A proactive approach helps to ensure that you are ready for any IRS study – and keep your focus on what really matters: your cryptoin investments.

See here for the full article and more detailed guidance.