Bitcoins volatility indices are still falling, mirroring those in the S&P 500, bringing price stability that weakens the case for a year-end rally, according to one analyst.

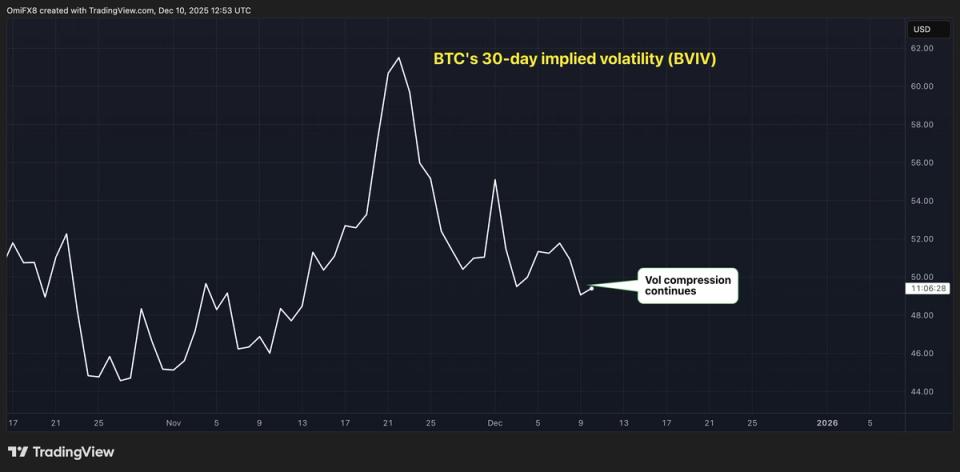

BTC’s annualized 30-day implied volatility, as measured by Volmex’s BVIV index, has fallen to 49%, nearly reversing a rise to 65% from 46% over the 10 days through Nov. 21, according to TradingView data.

Implied volatility is an option-based measure that represents the market’s outlook for price fluctuations over a specified period of time. The drop from 65% to 49% means that the expected price turbulence over the 30 days has dropped from as much as 5 percentage points to 14%.

The VIX index, which represents the 30-day implied volatility of the S&P 500, has also fallen, reaching 17% from 28% since November 20.

According to Matrixport, the so-called volatility compression suggests low odds of a year-end rally.

“Implied volatility continues to compress, and with it, the likelihood of a meaningful year-end upside breakout,” the firm said in a market update on Wednesday. “Today’s FOMC meeting represents the last major catalyst, but once that passes, volatility is likely to slide lower into the end of the year.”

Matrixport’s view is consistent with bitcoin’s historical positive price-volatility correlation, although this relationship has gradually shifted towards the negative since November 2024.

On Wall Street, implied volatility compression is typically associated with a bullish reset in market sentiment.