Bitcoin’s (BTC) volatility melting continues as cryptocurrency remains stagnant with slow price between $ 110,000 and $ 120,000.

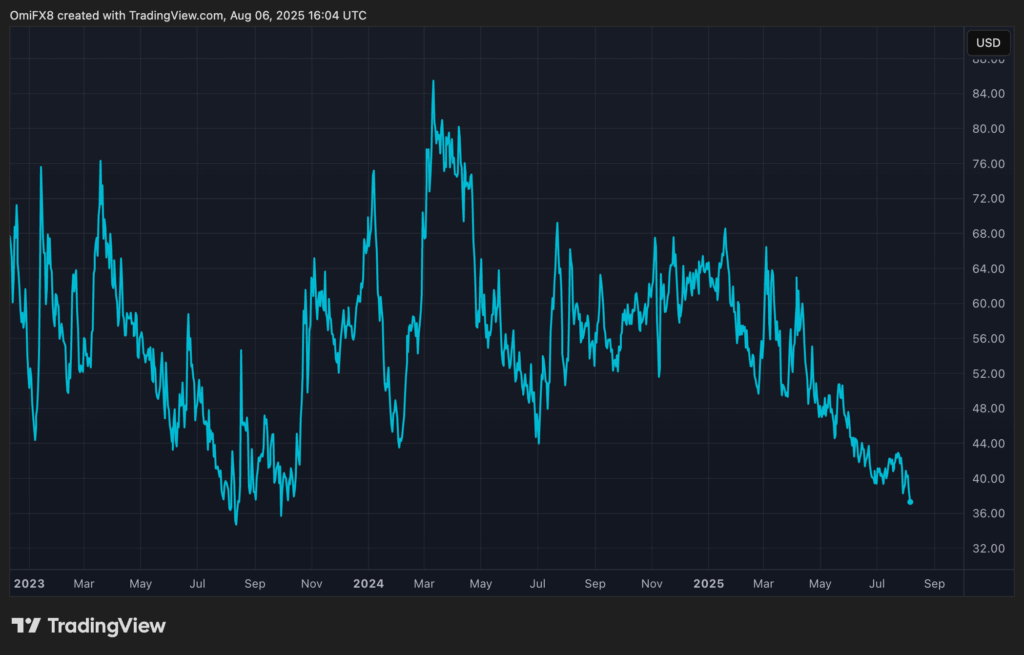

Cryptocurrency’s 30-day implicit volatility, represented by Volmex’s BVIV index, dropped to an annual 36.5% late Wednesday and reached levels last viewed in October 2023, when BTC traded under $ 30,000, according to Data Source Tradingview.

The new perennial low in implied volatility suggests that trade dealers are not yet rushing to hedges, despite the fact that US financial data raises concerns about stagflation. The demand for options that are contracts used to uncover the courage or profit from price fluctuations is an important driver of an asset’s implicit volatility.

The same thing can be said of shares where the VIX index has turned Friday’s increase from 17 to 21. VIX measures the 30-day implicit volatility in the S&P 500.

BTC mirrors the stock market’s volatility patterns

BTC’s implied volatility has been downwardly downward, moved in the opposite direction of Cryptocurrency’s award, which has risen from $ 70,000 to over $ 110,000 since November.

The negative correlation marks an in -depth shift in Bitcoin’s market dynamics. Historically, BTC’s volatility and its spot price in tandem moved, with volatility rising in both bull and bear markets.

The change in this spot volatility correlation is partly attributed to the growing popularity of structured products involving writing (sales) of call options for the money, analysts told Coindesk.

This new dynamic suggests that Bitcoin is increasingly mirroring patterns on Wall Street, where suggested volatility often subsides during stable bull races.

Read: Bitcoin’s ‘Low Volatility’ Rally from $ 70k to $ 118K: A tale of transition from Wild West to Wall Street-like dynamics