Ethereum is in the middle of a paradox. Even when Ether hit record highs in late August, decentralized funding (defi) sees activity at Ethereum’s LAG-1 (L1) muted out compared to its peak at the end of 2021. Fees collected on Mainnet in August were only $ 44 million, a fall of 44% from the previous month.

Meanwhile, LAG-2 (L2) is blooming networks such as arbitum and base with $ 20 billion and $ 15 billion respectively in the total value locked (tvl).

This divergence raises a crucial question: L2’s cannibalizing Ethereum’s defi activity, or does the ecosystem develop into a multi-layer financial architecture?

AJ Warner, Chief Strategy Officer for Offchain Labs, the developer company behind Layer-2 Arbitum, claims the measurements are more nuanced than just Layer-2 Defi Chipping in Layer 1.

In an interview with Coindesk, Warner said that focusing solely on Tvl is missing out on the point and that Ethereum is increasingly acting as Crypto’s “global settlement layer”, a foundation for the issuance of high value and institutional activity. Products such as Franklin Templeton’s Tokenized Funds or Blackrocks Buidl -Product Launch Directly on Ethereum L1 -activity not fully trapped in Defi -Metrics, but emphasizes Ethereum’s role as the cornerstone of crypto -tofanance.

Ethereum like Layer-1 Blockchain is the safe but relatively slow and expensive basic network. LAG-2’s scales networks built on top of it, designed to handle transactions faster and to a fraction of the costs before eventually running an Ethereum for security. Therefore, they have become so appealing to both traders and builders. Metrics like Tvl, the amount of crypto deposited in defi protocols highlights this shift when the activity is moved to L2s, where lower fees and faster confirmations make everyday life defi far more practical.

Warner compares Ethereums Square in the ecosystem with a thread transfer in traditional financing: trusted, secure and used for large -scale settlement. However, everyday transactions are migrating to L2S – Venmos and PayPals of Crypto.

“Ethereum would never become a monolithic blockchain with all the activity happening on it,” Warner told Coindesk. Instead, it is intended to anchor security while allowing rollups to perform faster, cheaper and more different applications.

LAG 2S, which has exploded in the last few years because they are seen as the faster and cheaper alternative to Ethereum, enables entire categories of defi that do not work so well on the mainnet. Quick trading strategies, such as arbitration price differences between exchanges or continuous eternal futures, do not work well on Ethereum’s slower 12-second blocks. But at Arbitum, where transactions end in a second, the same strategies become possible, Warner explained. This appears as Ethereum has had fewer than 50 million transactions over the past month compared to Base’s 328 million transactions and Arbitum’s 77 million transactions, according to L2Beat.

Builders also see L2S as an ideal test space. Alice Hou, a research analyst at Messari, pointed to innovations such as Uniswap V4’s hooks, customized features that can be much cheaper on L2S before going mainstream. For developers, faster confirmations and lower costs are more than a convenience: they expand what is possible.

“L2s provide a natural playground to test these kinds of innovations, and when a hook achieves breakout popularity, it could attract new types of users who engage in defi in ways not possible on L1,” Hou said.

But the shift is not just about technology. Liquidity providers respond to incentives. Hou said data is showing smaller liquidity providers increasingly prefer L2s, where dividends and lower sliding reinforcement returns. However, larger liquidity providers still cling to Ethereum, prioritizing the security and depth of liquidity over greater yields.

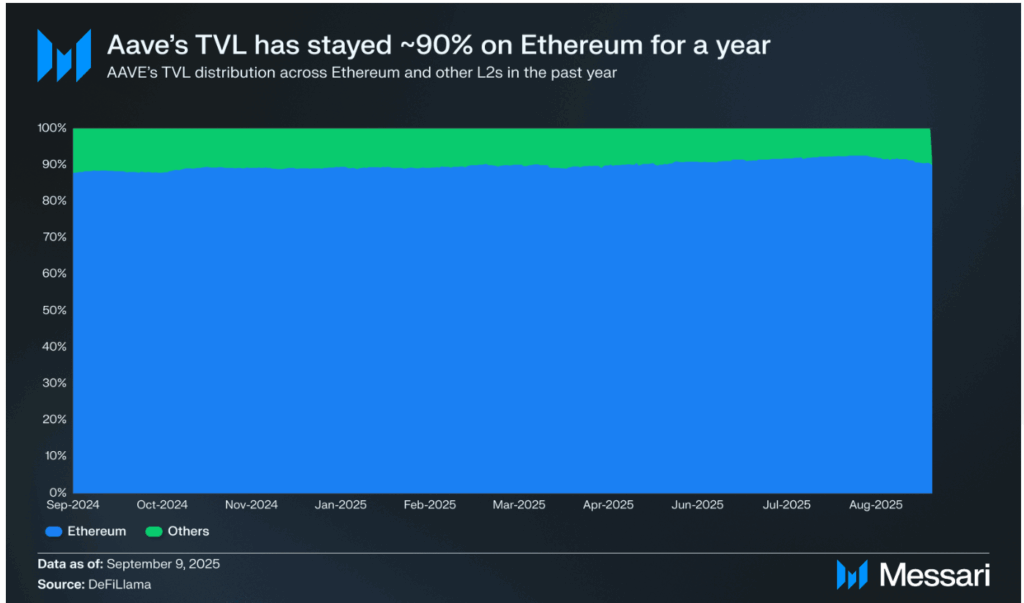

Interestingly, while L2S catches more activity, the flagship defi -protocols such as Aave and Uniswap are still strong on the mainnet. Aave has consistently kept about 90% of his tvl at Ethereum. With Uniswap, however, there has been a step -by -step shift against L2 activity.

")

Another factor that accelerates L2 -recording is user experience. Wallets, bridges and Fiat on ramps are increasingly managing newcomers directly to L2S, Hou said. Ultimately, the data suggests that L1 vs. The L2 debate is not zero-sum.

From September 2025, about one -third of L2 Tvl is still bridging from Ethereum, another third is natively mint and the rest comes via external bridges.

“This mixture shows that although Ethereum remains a key source for liquidity, L2S also develops their own original ecosystems and attracts crossed assets,” Hou said.

Ethereum thus, as a base layer, seems to cement itself as the safe settlement engine for global funding, while Rollups like Arbitum and Base emerge as execution layers for fast, cheap and creative defi applications.

“Most payments I make use something like Zelle or PayPal … But when I bought my home, I used a cord. It’s a bit parallel to what happens between Ethereum Layer One and Layer Twos,” said Warner of Offchain Labs.

Read more: Ethereum Defi delays, even when the Ether Price crossed record heights