In the financial markets, Startups have long tried to market themselves as “tech companies” in the hope that investors will appreciate them with technical-business multipling. And often they do – at least for a while.

Traditional institutions learned this the hard way. During the 2010s, many companies shrinked to move themselves as technology companies. Banks, payment processors and retailers began to call themselves fintech’s or data companies. But few won valuation multipling from real tech companies – because the basic elements rarely matched the narrative.

WeWork was among the most notorious examples: a real estate company dressed up as a technical platform that eventually collapsed under the weight of its own illusion. In financial services, Goldman Sachs Marcus launched in 2016 as a digital first platform to compete with Consumer Finchs. Despite the early traction, the initiative was scaled back in 2023 by persistent profitability problems.

JPMorgan famously declared himself “a technology company with a banking license”, while BBVA and Wells Fargo invested strongly in digital transformation. Still, few of these efforts produced platform level produced. Today, there is a cemetery of such business-technical delusions-a clear reminder that no amount of branding can override the structural restrictions on capital-intensive or regulated business models.

Crypto now confronts a similar identity crisis. Defi protocols want to be appreciated as LAG 1’s. Real assets (RWA) DAPPs present themselves as superb networking. All chasing layer 1 “The Technology Prize.”

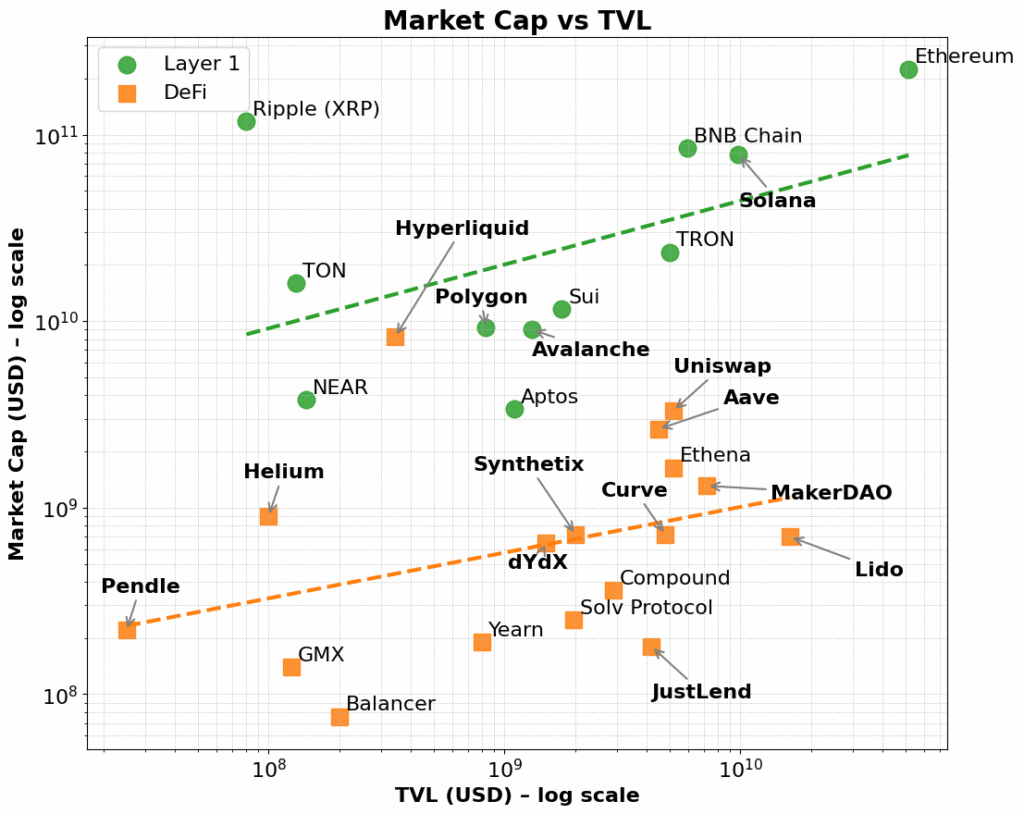

And to be fair – this prize is real. LAG 1 networks such as Ethereum, Solana and BNB consistently command Multipla with higher valuation in relation to measurements such as total value locked (tvl) and fee generation. They benefit from a wider market narrative – one that rewards infrastructure of applications and platforms of products.

This prize applies even when checking for basic elements. Many Defi Protocols demonstrate strong Tvl or Fee General, but are still struggling to achieve comparable market values. In contrast, LAG 1s attract early users through incentives for validator and native token economy and then expanded to developer ecosystems and composed applications.

Ultimately, this premium 1S ‘capacity for broad native token tool, ecosystem coordination and prolonged extension. As a fee volume grows, these networks often see disproportionate increases in market value – a sign that investors prices in not only current use but future potential and compound network effects.

This layered flywheel, moving from the adoption of infrastructure to growth in the ecosystem, helps to explain why layers consistently command higher valuations than DAPPs, even when underlying performance metrics appear to be the same.

This reflects how stock markets separate platforms from products. Infrastructure companies such as AWS, Microsoft Azure, Apple’s App Store or Meta’s developer ecosystem are more than service providers – they are ecosystems. They allow thousands of developers and businesses to build, scale and interact. Investors award higher multiples not only for current revenue, but for the potential to support new use cases, network effects and economies of scale. In contrast, even very profitable SaaS tools or niche services rarely attract the same valuation prize -their growth is limited by limited API composability and narrow utility.

The same pattern now plays out among the Large Language Model (LLM) providers. Most people run to place themselves as chatbots, but as basic infrastructure for AI applications. Everyone will be AWS – not Mailchimp.

LAG 1s in crypto follow a similar logic. They are not just blockchains; They are coordination layers for decentralized calculation and state synchronization. They support a wide range of composed applications and assets. Their native tokens accrue value through basic layering activity: gas fees, stacking, mev and more. Of crucial importance, these tokens also act as mechanisms to incentive developers and users. Layer 1S takes advantage of self-reinforcing loops between users, builders, liquidity and demand for token and they support both vertical and horizontal scaling across sectors. Read the full article here.

Most protocols, on the other hand, are not infrastructure. They are one-target products. So adding a validator set doesn’t get them to layer 1’s – it simply dresses a product in infrastructure optics to justify a higher valuation.

This is where the Appchain trend comes into the picture. Appchains combine application, protocol logic and a settlement layer in a vertically integrated stack. They promise better fees, user experience and “sovereignty.” In a few cases – like hyperliquid – they deliver. By controlling the full stack, Hyperliquid has achieved quick execution, excellent UX and meaningful fee generation – all without relying on tokenincitaments. Developers can even implement DAPPs on its underlying layer 1 and take advantage of its high performance decentralized exchange infrastructure. While its scope remains narrow, it gives a glimpse of a certain level of wider scaling potential.

But most appchains are simply protocols trying to redirect, with little use and no ecosystem depth. They are fighting a two-front war: trying to build both infrastructure and a product at the same time, often without capital or team to do it neither good. The result is a blurry hybrid-not a performing layer 1 and not a category-defining DAPP.

We’ve seen this before. A robo advisor with a smooth user interface was still a wealth manager. A bank with open APIs was still a balance business. A coworking company with a polished app was still just renting office space. Eventually, the hype goes off – and the market environment accordingly.

RWA protocols now fall into the same trap. Many people place themselves as infrastructure for tokenized funding – but without meaningful differentiation from existing layers 1s or sustainable user recording. At best, the vertically integrated products are without a convincing need for a superbly settlement layer. Worse is that most people have not achieved product market that fits into their core use case. They bolt on infrastructure and lean into inflated tales in the hope of justifying valuations that their finances cannot support.

So what’s the path forward?

The answer is not to false infrastructure status. It is to own your role as a product or a service – and perform the unusually good. If your protocol solves a real problem and drives meaningful Tvl growth, it is a strong foundation. But Tvl alone doesn’t make you a successful appchain.

What matters most is real economic activity: Tvl, which drives sustainable fee generation, user storage and clear value accrual to the native token. In addition, if developers are based on your protocol because it is really useful – not because it claims to be infrastructure – the market will reward you. Platform status is earned, not claiming.

Some defi protocols – like maker/cloud and uniswap – follow this path. They develop against appchain-style models that improve scalability and cross-network access. But they do it from a position of strength: with established ecosystems, clear income and product market.

In contrast, the new RWA room has not yet demonstrated durable traction. Almost every RWA protocol or centralized service rushes to launch an appchain – often supported by fragile or untested economy. As with leading defi protocols that switch to an appchain model, the best path forward to RWA protocols is to first utilize existing layers 1 -o -ecosystems, build user and developer traction leading to Tvl growth, demonstrating sustainable fee generation and only then developing against an appchain -infrastructure model -with a clear purpose and strategy.

Therefore, in the event of an appchain, the tool and the economy of the underlying application must come first. Only when proven makes a transition to a superb layer 1 viable. This is in contrast to the growth track for the general purpose LAG 1s, which can initially prioritize the construction of a validator and the trader ecosystem. Early generation of the fee is driven by native token transactions, and over time the cross market scaling is expanding the network to include developers and end users -ultimately to operate Tvl growth and diversified fee flows.

As crypto matures, fog is lifted by storytelling and investors become more discerning. Buzzwords such as “Appchain” and “Layer 1” no longer commands attention on your own. Without a clear value proposition, sustainable token economy and a well -defined strategic course, protocols lack the basic elements required for any credible transition to genuine infrastructure.

What Krypto needs – especially in the RWA sector – are no more layers 1’s. It needs better products. And the market will reward those who focus on building exactly it.

Figure 1. Market hood vs tvl for defi and layer 1S

Figure 2. Layer 1S is assembled around higher fees and dapps around lower fees