With only about 20% of the $10.6 billion in open interest sitting in-the-money (ITM) and the remaining 80% out-of-the-money (OTM), the market has a strong imbalance that can generate sharp price swings as participants struggle to adjust their positions.

The story does not end there.

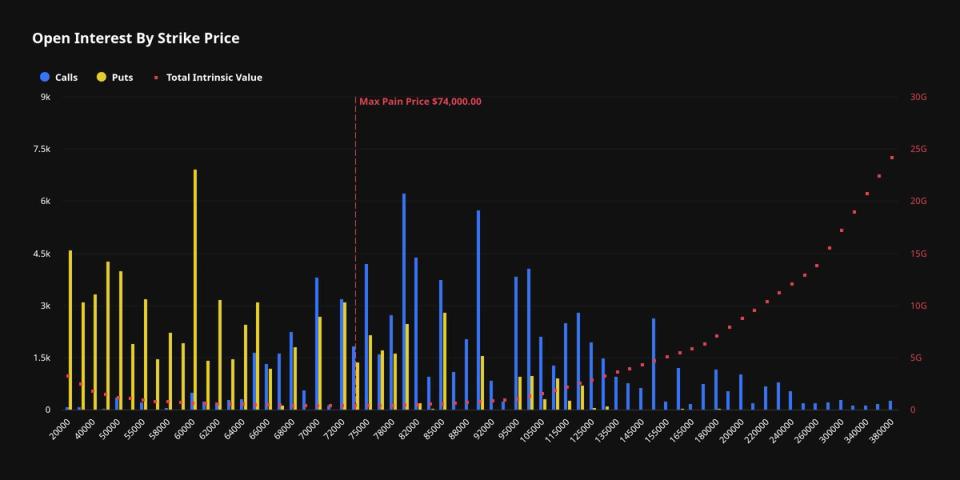

Max pain and put-call ratio

Another factor pointing to potential volatility is the maximum pain price for the June 26 expiration, which currently stands at $74,000, about 14% above bitcoin’s current spot price near $65,000.

Max pain is the price level at which the largest number of option contracts would expire completely worthless. The theory suggests that as expiration approaches, the underlying asset (in this case, bitcoin) tends to gravitate toward the maximum pain level as market makers and traders adjust their positions.

While this “max pain” effect is widely seen in traditional markets, its reliability in crypto is often debated. Still, if the theory holds, bitcoin could see a strong jump towards $74,000 in the coming days.

Meanwhile, the put-to-call ratio is 0.87, reflecting 87,156 call contracts versus 76,241 put contracts on more than $10.6 billion in nominal open interest. Although call options are still slightly larger than puts, the relatively balanced positioning highlights growing uncertainty among traders.

Open interest is heavily concentrated around two key attacks. The $60,000 put holds about $450 million in exposure, making it an important support level that bitcoin tested in early June. Meanwhile, the $80,000 call, with about $406 million in open interest, remains a significant upside hurdle.