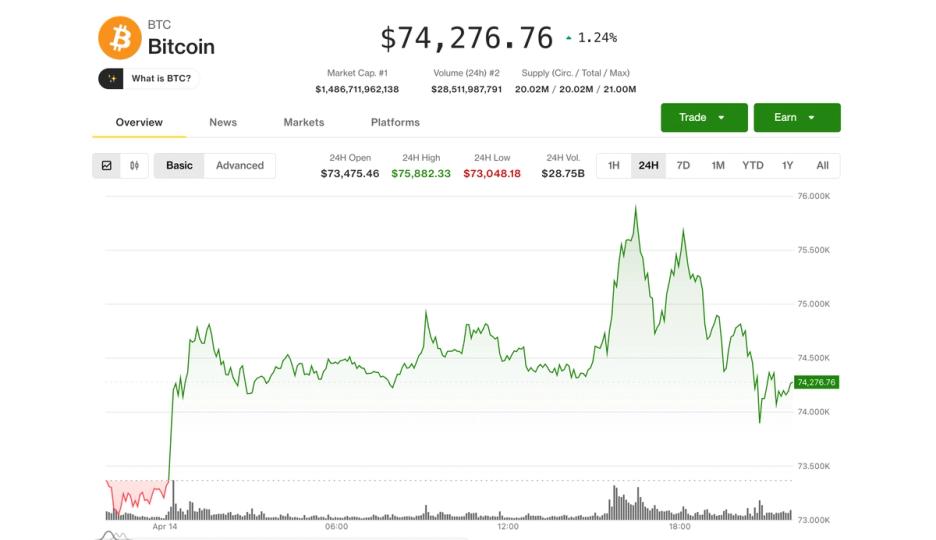

Bitcoin started the day with a promising chance for a breakout, but the rally ran out at a familiar brick wall that has kept a lid on prices for more than two months.

After briefly topping $76,000 – a key resistance level – the largest cryptocurrency reversed and fell below $74,000 later in the session. It still held on to a 1.3% gain over the past 24 hours, and recently changed hands near $74,300.

Ether (ETH) followed a similar path, retreating from above $2,400, but still outperformed, rising 2.5% daily. Traditional markets saw no such reversal, with the Nasdaq closing at its session high, up 2%.

Still, conditions are ripe for a push higher, even if Tuesday’s breakout didn’t last.

According to Vetle Lunde, head of research at K33 Research, funding rates on Binance’s bitcoin perpetuals have remained negative for 11 consecutive periods despite the recent rally, signaling that traders are still leaning bearish even as prices push up. At the same time, open interest has been increasing, suggesting new short positions are being added rather than being closed, he said.

That combination has historically set the stage for sharp upward moves, he said.

The 30-day average funding rate has now been negative for 46 days in a row, Lunde added, matching the extended bearish positioning seen during previous periods of market stress, such as after the FTX crash in late 2022 and the mid-2021 bear market when China banned bitcoin mining.

“Comparable risk-off regimes have historically been attractive entry points for BTC,” Lunde said as crowded short traders were forced to unwind.