A Pakistani software engineer in Toronto wants to invest $200 in OGDC. A fund manager in Singapore has been tracking the KSE-100 for two years and is looking for a way to build exposure. A family office in Dubai that distributes frontier markets has Pakistan on its watch list, but no practical mechanism to respond to this conviction.

None of them can invest without navigating a maze of currency accounts, fragmented brokerage processes and settlement systems built for a bygone era. This is not a diaspora problem but a demand problem. The capital is there, the interest is there too, and the market has earned it. What is missing is a simple way to act.

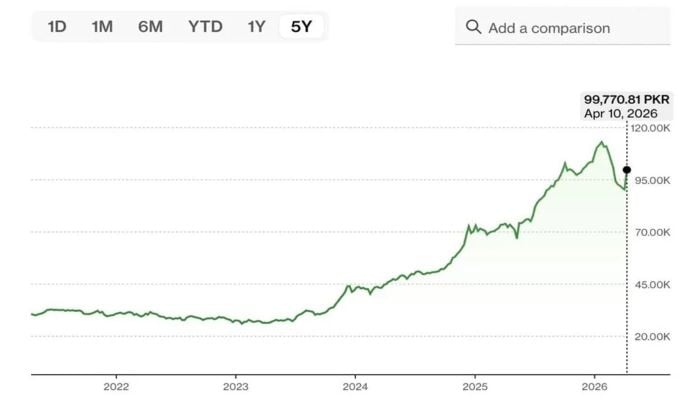

Over the past three years, Pakistan’s stock market has quietly become one of the strongest performers in the world. The KSE-100 returned over 50% last year and global allocators are starting to pay attention. When a market starts to outperform, curiosity follows. And curiosity always leads to the same question: How do I invest in it?

Right now there is no simple answer. What investors encounter instead is friction, layers of operational complexity that turn interest into hesitation and conviction into passivity.

Pakistan’s challenge is often misunderstood. We have 450,000 equity investors in a country of 250 million people. Domestic participation is limited, and the 6.9 million Pakistanis living abroad send back over $38 billion annually, yet invest almost none of it in the local stock market. And the growing pool of international investors who are paying attention have no clear entry point either. Look closely and these are not three different problems. They are domestic investors not participating, overseas Pakistanis unable to invest and global capital unable to enter. It is a simple problem with three pages. The problem is access.

Pakistan does not have an investment problem. It has an access problem, and access determines valuation.

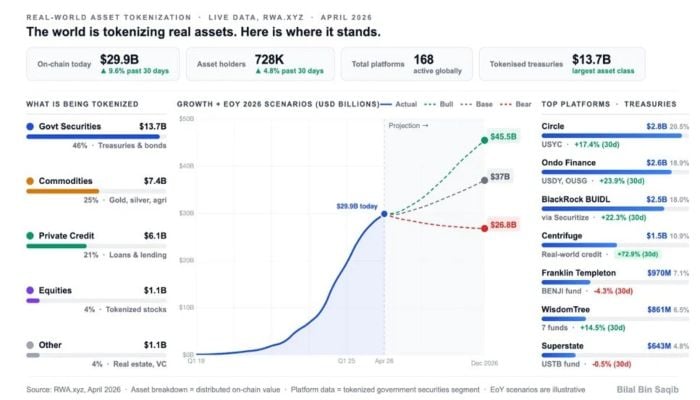

The global context in which this is situated matters. We are living through the early stages of the biggest restructuring of the capital markets since the creation of the stock exchange. Larry Fink, whose firm BlackRock manages nearly $150 billion in assets linked to digital products and runs the world’s largest tokenized fund, described it clearly in his 2026 annual letter to shareholders: tokenization, he wrote, is roughly where the Internet was in 1996, and the plumbing of the global financial system to allow any asset to be stored in any kind of wallet.

The numbers behind this thesis are significant. The global bond market alone stands at $140 trillion. Global equities add another $100 trillion to that, and private credit, real estate, commodities and infrastructure further expand the addressable universe. Simply put, tokenization turns assets such as stocks, fixed income instruments or real estate into digital entities that can be accessed from anywhere.

At that scale, the tokenized share of real-world assets today stands at $30 billion, up 9.6% in the last 30 days alone. BlackRock, Franklin Templeton, Circle, Ondo, Centrifuge. One hundred and sixty-eight platforms are live globally across all major asset classes. This is not one company or one jurisdiction making a speculative bet. It is the beginning of the largest capital migration in history, and the direction is not in doubt.

This matters most for markets like Pakistan. Frontier markets do not trade at a discount simply because of fundamentals; they trade at a discount because the pool of potential buyers is limited. Limited access narrows participation, and narrow participation suppresses valuation. Access is not a detail; it is a requirement, and unlike many structural challenges, it is one of the most solvable.

As the barriers to entry fall, the dynamic changes. The same investor who can buy Apple or Saudi Aramco from a single interface should be able to buy OGDC or HBL with equal ease. As it becomes possible, Pakistani companies are no longer competing only for domestic capital but for allocation from a global pool.

The effect is straightforward: more access leads to more participants, more participants leads to stronger demand discovery, stronger demand supports fairer valuations, better valuations lower the cost of capital – and this is how access becomes capital formation.

This is where the opportunity becomes tangible. Instead of asking global investors to navigate local complexities, Pakistan can present itself through simple, globally readable products. For example, a curated basket of leading Pakistani companies – an index that represents the country’s growth story. Digital wrappers that enable investors everywhere to gain exposure without rebuilding infrastructure from scratch. It is not about replacing the existing market; it will simply multiply the range exponentially.

It is also not only about Pakistanis abroad looking inward, but also about the world looking at Pakistan and for the first time finding a door that opens, and the diaspora is the natural starting point. Even if a small percentage of overseas Pakistanis allocate some of their capital through available instruments, the inflow alone would be significant. But that’s only the floor; the real opportunity begins when Pakistan becomes investable for anyone, anywhere who wants exposure.

As access improves, the effects are amplified. A wider investor base deepens liquidity, which then reduces perceived risk, and lower risk attracts more capital. And companies that grow with capital at a better price build the track record that brings the next wave of attention. Access and valuation reinforce each other and the markets that recognize this early advantage disproportionately.

Other jurisdictions have already moved in this direction. Singapore built a tokenization framework through Project Guardian in under two years, bringing together major financial institutions to test and implement new market infrastructure. The UAE has done the same within the DIFC.

Pakistan is already being noticed on all fronts. The performance is real and interest is growing with higher mindshare capture on all fronts. The engineer in Toronto, the fund manager in Singapore, the family office in Dubai, they don’t wait for a narrative; they await easier access.

Pakistan Stock Exchange has done its job. Sustained performance has placed the market on the global map. The next stage is not about proving the possibility; it’s simply about making that option available. Because in the capital markets, attention does not automatically translate into investment, access is what converts interest into capital.

And what lies on the other side of that access is bigger than just the diaspora sending money home. It is the integration of Pakistan into the very global flow of capital.

The author is the Chairman of Pakistan Virtual Assets Regulatory Authority (PVARA).

Disclaimer: The views expressed in this piece are the author’s own and do not necessarily reflect Pakinomist.tv’s editorial policy.

Originally published in The News